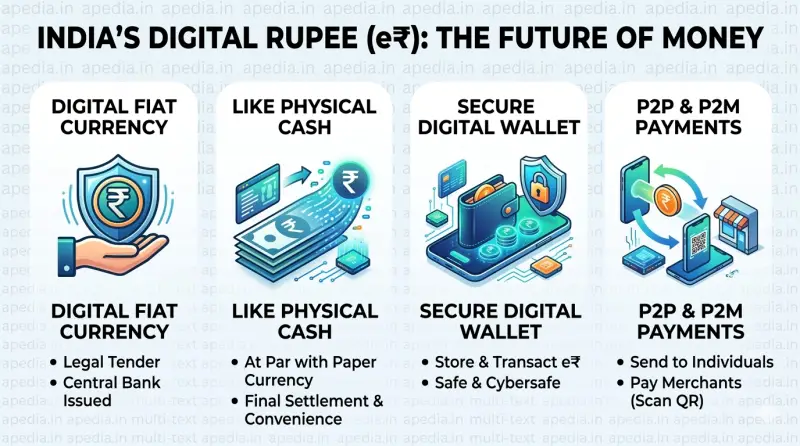

💧 Understanding India's Digital Rupee (e₹)

The Digital Rupee (e₹) represents a paradigm shift in India's monetary system, acting as the Central Bank Digital Currency (CBDC) issued by the Reserve Bank of India. Functioning as a sovereign digital equivalent of physical fiat currency, it carries the same legal tender status and sovereign guarantee. Unlike standard digital payments that rely on bank intermediaries, the e₹ acts as a direct store of value maintained in digital wallets. It is currently being piloted in two broad categories: Retail CBDC for everyday consumer transactions and Wholesale CBDC for institutional interbank settlements, pushing India toward a more frictionless, inclusive, and cost-efficient financial ecosystem.

💧 Key Initiatives & Strategic Focus

The Reserve Bank has engineered the e₹ framework with distinct capabilities to solve systemic inefficiencies in traditional digital finance.

- Restricted to financial institutions and intermediaries.

- Settles secondary market transactions in Government Securities (G-Secs).

- Facilitates inter-bank lending in the call money market.

- Dramatically reduces settlement risks and collateral requirements.

📚 UPSC CSE Quiz Corner

- A) It is recognized as legal tender under the provisions of the Reserve Bank of India Act, 1934.

- B) To encourage adoption, balances maintained in the e₹ wallet earn an interest rate equivalent to the standard savings account.

- C) It settles peer-to-peer (P2P) transactions directly between digital wallets without requiring intermediary bank routing.

- D) It offers programmability features, allowing the sponsor entity to restrict funds for specific, designated purposes.