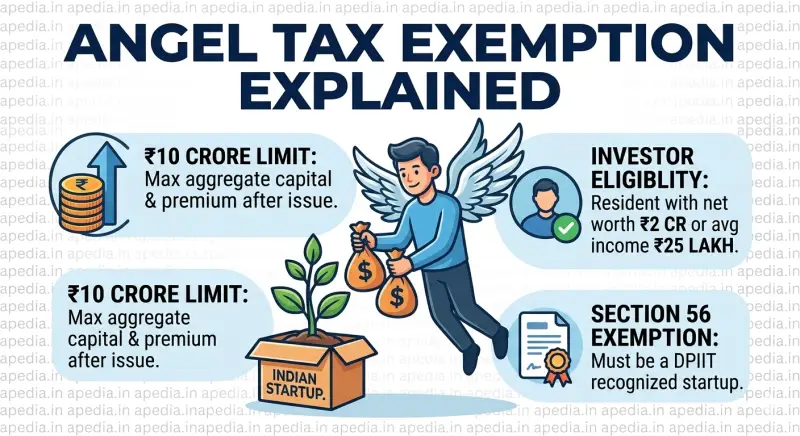

💧 Understanding the Angel Tax Exemption

India proudly stands as the world's third-largest ecosystem for startups, a feat heavily reliant on early-stage funding from angel investors. However, a major hurdle for emerging businesses has been the 'Angel Tax'—a tax levied on investments received by unlisted companies when the share price exceeds the firm's fair market value. Recognizing this challenge, the Department for Promotion of Industry and Internal Trade (DPIIT) recently rolled out vital notifications to exempt recognized private limited startups from this tax burden under Section 56 of the Income Tax Act.

₹10 Crore

Max Capital & Premium Limit

₹2 Crore

Investor Net Worth Requirement

88 Startups

Initially Certified for 80 IAC

💧 Key Eligibility & Procedural Guidelines

To claim this critical tax exemption on angel investments, specific parameters must be fulfilled by both the startup and its investors.

🏢 Startup Eligibility Criteria

The aggregate paid-up share capital and share premium of the startup, after the proposed issue of shares, must not exceed ₹10 crore.

💼 Investor Eligibility Rules

Any resident investor backing the startup must either have a minimum average returned income of ₹25 lakh for the preceding three financial years OR possess a minimum net worth of ₹2 crore as on the last date of the preceding financial year.

📑 The Application Process

- Startups must fill the 'Exemption under Section 56' application form.

- The application requires a fair market value report of shares (as per Rule 11UA) from a SEBI-registered Category-I merchant banker.

- Applications are evaluated by an 8-member Inter-Ministerial Board established by DPIIT.

- The board also reviews applications for a 3-year tax holiday under Section 80 IAC for eligible Private Limited or LLP companies.

📚 Prelims Quiz Corner

1. With reference to the 'Angel Tax Exemption' for startups in India, consider the following statements:

1. The aggregate amount of paid-up share capital and share premium of the startup after the proposed issue of shares must not exceed ₹100 crore.

2. The investing resident individual must have a minimum net worth of ₹2 crore as of the last financial year.

3. The application requires a valuation report from a SEBI registered Category-I merchant banker.

Which of the statements given above is/are correct?

1. The aggregate amount of paid-up share capital and share premium of the startup after the proposed issue of shares must not exceed ₹100 crore.

2. The investing resident individual must have a minimum net worth of ₹2 crore as of the last financial year.

3. The application requires a valuation report from a SEBI registered Category-I merchant banker.

Which of the statements given above is/are correct?

- A) 1 and 2 only

- B) 1 and 3 only

- C) 1 only

- D) 2 and 3 only

✓ Answer: D

Source Reference

Startup India | ID: DPIIT-AngelTax | 23-JAN-2026